Missing your HMRC tax tribunal appeal deadline doesn’t mean your case is over. The Upper Tax Tribunal’s landmark decision in Medpro Healthcare Ltd v HMRC [2025] UKUT 255 (TCC) fundamentally changed how tribunals approach late appeals, moving away from the strict Martland framework that previously barred most out-of-time applications. Today, tribunals weigh all circumstances equally, from delay length, reasons for lateness, and your case’s strength, rather than treating deadlines as near-absolute barriers. This shift opens new pathways for taxpayers with meritorious claims, but success depends on understanding the evolving rules and acting strategically with the benefit of expert tax disputes advice. This guide explains the current tribunal landscape and your practical options.

1. The Problem: Why Missed Appeal Deadlines Matter

HMRC decisions are not self enforcing, but time limits for challenging them are strict. In most cases you have 30 days to appeal an assessment, penalty or closure notice to the tax tribunal. If you miss that deadline, the decision becomes final unless the tribunal grants permission for a late appeal.

That matters for several reasons. First, once the deadline passes HMRC will treat the liability as fixed and will usually begin collection or enforcement. Second, evidence can deteriorate as time passes, witnesses become harder to locate and documents are more likely to be lost. Third, there is a public interest in finality. HMRC and the tribunal system are not expected to keep cases permanently open on the off chance that a taxpayer might reconsider their position months or years later.

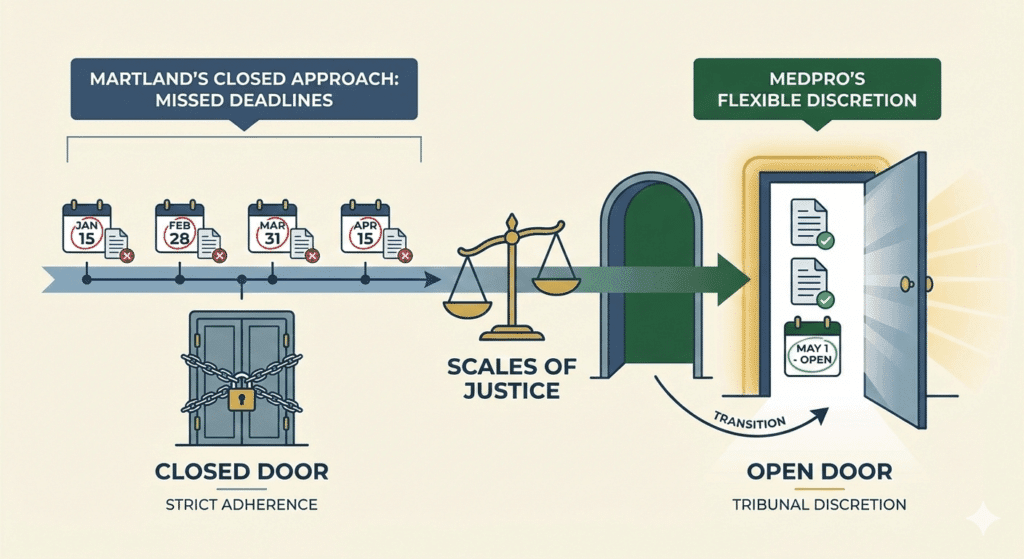

Historically, tribunals used missed deadlines as a relatively blunt instrument. In many cases, even where there appeared to be a good argument that HMRC was wrong on the substantive tax position, a weak explanation for the delay would lead to permission being refused. That was the environment created by Martland; however Medpro changes the balance and gives taxpayers with strong underlying cases a better prospect of rescuing a late appeal, provided they can present their circumstances clearly and credibly.

2. The Old Rule: Martland’s Three Stage Test (2018 to 2024)

For years, the starting point for late appeal applications was William Martland v The Commissioners for HM Revenue and Customs [2018] UKUT 0178 (TCC). Martland did not invent the law on late appeals, but it distilled tribunal practice into a structured three stage test that quickly became the default framework.

Under Martland, the tribunal asked:

- How long was the delay

- What were the reasons for the delay

- What are the merits of the proposed appeal

The first two questions were often decisive. The longer the delay, the more compelling the explanation needed to be. Modest delays could sometimes be forgiven with relatively ordinary reasons. Highly extended delays required exceptional circumstances.

In practice, Martland placed significant weight on procedural efficiency and the need for finality. The case was often read as saying that the merits of the appeal should carry less weight than the length of delay and the quality of the explanation. It was not enough for a taxpayer to show that HMRC might be wrong. If the reasons for missing the deadline were weak, the tribunal would usually refuse permission, sometimes even where the underlying tax dispute looked relatively strong.

This approach attracted criticism. Commentators and practitioners argued that it risked prioritising administrative neatness over substantive justice. A meritorious appeal could be shut out permanently because an agent miscalendared a date or because correspondence with HMRC drifted for longer than expected.

Even before Medpro, some decisions applied Martland more flexibly, but the overall tone was restrictive. Taxpayers were repeatedly reminded that the default position was to respect statutory deadlines. Medpro brought that approach into direct question at Upper Tribunal level.

3. The Shift: Medpro’s Game Changing Decision (2025)

Medpro Healthcare Ltd v HMRC reached the Upper Tribunal in 2025 as a challenge to the First tier Tribunal’s refusal to admit a late appeal. The facts of Medpro are important because they illustrate the kind of real world situation in which late appeals arise.

In outline, Medpro had missed the appeal deadline against an HMRC decision. There was a gap between the decision being issued and the formal appeal being lodged, and HMRC argued that the delay was unjustified. The First tier Tribunal applied the Martland framework and refused permission, treating the delay and explanation as insufficient to overcome the emphasis on time limits.

On appeal, the Upper Tribunal took a much harder look at the underlying approach. It found that Martland had effectively elevated certain considerations, especially the importance of finality and the efficient running of the tribunal system, above the statutory test that simply requires the tribunal to consider whether to admit a late appeal in all the circumstances.

The Upper Tribunal described the Martland approach as clearly wrong to the extent that it fettered the discretion conferred on the tribunal. The law did not require a hierarchy where delay and reasons dominate, with merits playing only a secondary role. Instead, the tribunal is required to exercise a broad discretion, weighing all relevant factors without pre ordaining which will usually prevail.

The decision in Medpro therefore does two important things:

First, it confirms that the merits of the underlying tax appeal can be a powerful factor in favour of admitting a late appeal. If HMRC’s decision is seriously vulnerable on the law or the facts, the tribunal should not ignore that simply because there has been an administrative failure on timing.

Second, it resets the mindset about time limits. They are still important and cannot simply be ignored, but they are not near absolute barriers. The question is not whether the taxpayer can meet a Martland style threshold. The question is whether, taking everything into account, justice is better served by hearing the appeal than by shutting it out.

For taxpayers and advisers, Medpro marks a significant softening of the hostile environment created by Martland. It does not guarantee that late appeals will be allowed, but it plainly gives more scope to rescue valid disputes where the deadline was missed for understandable reasons.

4. How Tribunals Decide Now: The Post Medpro Test

Post Medpro, there is no rigid formula. The tribunal must consider all the circumstances and then decide whether, in the exercise of its discretion, it should permit a late appeal. Nevertheless, certain themes now emerge consistently from tribunal decisions.

Tribunals will usually look at:

- The length of the delay

- The reasons for the delay

- The merits of the proposed appeal

- The prejudice to HMRC if the appeal is admitted late

- The prejudice to the taxpayer if the appeal is barred

- The broader public interest in finality and efficient administration

Crucially, none of these factors is automatically dominant. A relatively long delay may still be excusable if there is a persuasive reason and a strong case. A relatively short delay may still result in refusal if the explanation shows cavalier disregard for statutory time limits and the appeal appears weak.

In practical terms, the reasoning often follows a pattern.

If the delay is modest and the explanation is reasonable, tribunals are now more willing to admit late appeals even where the merits are arguable rather than overwhelming. If the delay is substantial, tribunals will scrutinise both the explanation and the underlying case more closely. Where the taxpayer can show that HMRC’s decision is clearly wrong, Medpro suggests that the tribunal should be slow to prevent the appeal from being heard purely on timing grounds.

Examples since Medpro show both outcomes.

Some taxpayers have succeeded where they acted promptly once they realised the missed deadline, could evidence confusion caused by HMRC correspondence or professional advice, and could demonstrate a credible argument that the assessment or penalty was unlawful. Other taxpayers have still failed where the delay was extensive, the explanation amounted to little more than administrative disorganisation, and the underlying case was weak or speculative.

The post Medpro test is therefore not a licence to ignore time limits. It is a more balanced approach that asks whether justice is better served by hearing the appeal or by enforcing finality.

5. Your Strength Factors: When Late Appeals Succeed

To assess the prospects of a late appeal, it helps to break down the main strength factors that tribunals find persuasive.

Strong reasons for delay

Tribunals are more sympathetic where the taxpayer can point to:

- Misleading or confusing HMRC correspondence that reasonably suggested that an appeal could be made later or that the dispute was still under review

- Reliance on professional advice where the adviser failed to file the appeal in time, particularly where the taxpayer can evidence instructions and follow up

- Serious illness, incapacity or personal circumstances that made it unrealistic to deal with tax matters within the deadline

- Genuine uncertainty about the correct route of challenge, for example where multiple overlapping decisions and internal HMRC review processes created confusion

These reasons do not guarantee success, but they provide a credible narrative that the taxpayer was not simply ignoring statutory obligations.

Weak reasons for delay

By contrast, tribunals are usually unimpressed by explanations such as:

- Forgetting the date with no mitigating circumstances

- Filing systems that were not maintained

- Staff turnover or holidays without adequate handover

- A general dislike of dealing with HMRC or hope that the issue would disappear

Such factors suggest a lack of due diligence rather than genuine difficulty. In combination with a weak underlying case, they make permission unlikely.

Strength of the underlying case

Medpro elevates the importance of the merits. Tribunals are more willing to admit late appeals where the taxpayer can show:

- A clear error of law in HMRC’s decision

- A misapplication of statute or guidance

- A factual misunderstanding that is objectively provable

- A consistent line of case law that favours the taxpayer’s position

On the other hand, if the proposed appeal depends on speculative arguments, incomplete evidence, or an attempt to re run points already rejected in internal review, the tribunal is less likely to take the risk of undermining finality.

A realistic assessment of these strength factors is essential before deciding whether to pursue a late appeal. It may be better to focus on negotiation or alternative remedies if the explanation and merits are both weak.

6. Building Your Case: Practical Steps

If you have missed a deadline and are considering a late appeal, preparation is critical. The tribunal will see only what you put before it. A late appeal application should therefore be treated as a substantive piece of litigation, not as a casual request.

Practical steps include:

- Document the timeline immediately

Write out a clear chronology showing key dates. For example, when HMRC issued its decision, when it was received, when you first considered appealing, what communications took place, and when you became aware that the deadline had been missed. Attach copies of correspondence where possible. - Explain the reasons for delay in concrete terms

The tribunal prefers specific facts to vague generalities. If you relied on an accountant, annex emails showing instructions. If illness was involved, obtain medical evidence. If HMRC communications were confusing, exhibit the letters. The more objective your explanation, the more credible it appears. - Set out the merits of your case succinctly

A late appeal application should include a summary of the grounds of appeal. This does not need to be a full skeleton argument, but it should show that there is a real prospect of success. Identify the core legal or factual error in HMRC’s position, and reference any supporting case law or statutory provisions. - Assess the financial stakes

Quantify the tax, penalties and interest involved. Tribunals are more willing to hear disputes where the sums are significant and the consequences for the taxpayer are serious. This does not mean small cases are hopeless, but proportionality is relevant. - Consider initial engagement with HMRC

In some situations, it is worth writing to HMRC first to explain the position and seek agreement to an out of time appeal. HMRC cannot waive statutory deadlines but can sometimes support or not oppose a late appeal where circumstances justify it. Evidence of constructive dialogue can assist before the tribunal. - Seek specialist advice

Given the complexity of Medpro and the discretionary nature of late appeal decisions, obtaining advice from a tax disputes specialist is often cost effective. A well framed application at the outset may avoid years of further litigation.

7. Your Options Beyond a Late Appeal

A formal late appeal to the tax tribunal is not the only possible route. Depending on your circumstances, other options may be available alongside or instead of an application to admit an out of time appeal.

HMRC statutory extension requests

In some contexts, HMRC has statutory power to agree an extension of time for appeal before the matter reaches the tribunal. For example, in VAT cases Regulation 36 of the VAT Regulations 1995 allows HMRC to extend certain time limits where there is a reasonable excuse and the taxpayer acts without unreasonable delay after the excuse has ended. Similar principles can arise under section 49 of the Taxes Management Act 1970 for direct tax appeals.

If you realise that you are close to, or slightly past, a deadline, it may be quicker and cheaper to seek an extension directly from HMRC. A carefully drafted request that mirrors the factors discussed above can sometimes resolve timing issues without the need for a formal tribunal application. However, HMRC is not obliged to grant an extension and may refuse, especially where delays are long or explanations are weak. A refusal does not prevent you from requesting a late appeal from the tribunal, but the tribunal will see the HMRC correspondence.

Judicial review of HMRC’s refusal

In rare cases, it may be appropriate to consider judicial review of HMRC’s refusal to extend time. This is a high threshold remedy, usually reserved for situations where HMRC has acted irrationally, ignored relevant factors, or applied its powers in a way that is legally flawed. Judicial review is not a rerun of the merits of the tax dispute. It is a challenge to the lawfulness of HMRC’s decision making process.

Because judicial review proceedings are expensive and carry cost risks, they are generally used only where large sums or important issues are at stake and where there is a strong argument that HMRC has misdirected itself. For most taxpayers, the focus will remain on the tribunal’s discretion in relation to a late appeal.

Settlement negotiations and alternative resolution

Even where a late appeal looks difficult, it may still be possible to negotiate with HMRC. In practice HMRC often prefers to resolve disputes through agreement rather than through lengthy litigation, especially where there is some litigation risk on both sides.

Depending on the stage of your case, options may include:

- Offering a partial settlement that reflects litigation risk

- Seeking a time to pay arrangement if the dispute is more about cash flow than underlying liability

- Engaging with HMRC’s alternative dispute resolution processes where available

The existence of Medpro may itself be a factor in negotiations. If HMRC recognises that a tribunal might be willing to admit a late appeal because of strong merits and a reasonable explanation, it may be more open to compromise.

8. Strategic Checklist: Am I Ready for a Late Appeal?

Before committing time and cost to a late appeal application, it is worth running through a simple strategic checklist. Honest answers to the following questions can save significant effort.

Credibility test

Can you explain, in a page or less, why the deadline was missed in a way that would make sense to an objective judge who knows nothing about your business? If the explanation sounds vague, inconsistent or casual, you may need to do more work to gather evidence or reconsider your approach.

Merits test

If you had appealed on time, would you have had a realistic chance of success on the substantive dispute? If the answer is no, or if your argument depends mainly on moral fairness rather than legal or factual error, a late appeal is unlikely to be a good use of resources.

Cost benefit test

Is the tax at stake significant compared to the costs of preparing and presenting a late appeal? Factor in tribunal fees, professional costs and management time. A principled fight may still be justified in some cases, but decisions should be made with clear eyes.

Timeline test

How long after the original deadline are you now? A delay measured in days or a few weeks is generally easier to justify than one measured in many months or years. Longer delays are not automatically fatal after Medpro, but they do increase the burden on you to show a persuasive explanation and strong merits.

If, after working through this checklist, you consider that your reasons are credible, your case is strong, the financial stakes are material and the delay is explainable, then a late appeal may be worth pursuing, particularly in the more flexible post Medpro environment.

9. Frequently Asked Questions

Common Queries on Late HMRC Tax Tribunal Appeals

Q1. How long can I wait before applying for a late appeal?

There is no fixed outer limit in the legislation. In theory, even very late appeals can be admitted. In practice, the longer the delay, the stronger your explanation and merits must be. A delay of a few weeks may be relatively straightforward to justify. A delay of several years will require exceptional circumstances and a very strong underlying case.

Q2. Will a strong case guarantee permission to appeal late?

No. Medpro confirms that merits are important, but they do not override everything else. A very strong tax case can help tip the balance, especially where the delay is moderate and the reasons are understandable. However, if the tribunal concludes that there was a serious and unjustifiable disregard of statutory time limits, permission can still be refused.

Q3. Can I appeal late if HMRC’s actions caused me to miss the deadline?

Possibly. If HMRC correspondence was unclear, contradictory or gave a reasonable impression that formal appeal could be made later, this can be a powerful explanation for delay. You will need to evidence exactly what was said and when. Tribunals are more receptive where the taxpayer relied on statements or implications from HMRC itself.

Q4. What is the difference between Medpro and Martland in plain English?

Martland encouraged tribunals to treat time limits as almost paramount. If you were significantly late without an excellent excuse, your chances were poor even if your tax case was strong. Medpro criticises that approach and tells tribunals to step back and look at the whole picture. Time limits still matter, but they are one important factor among several, not an automatic barrier.

Q5. Do I need a solicitor for a late appeal application?

You are not required to have a solicitor. Many taxpayers represent themselves. However, late appeal applications involve both procedural and substantive issues, and the tribunal will expect a clear explanation and coherent grounds of appeal. A specialist can help present your case in the most effective way, identify legal arguments you may have missed, and ensure that the application addresses the factors that tribunals consider relevant post Medpro.

Q6. How much does a late appeal cost?

There are two elements: tribunal fees and professional costs. Tribunal fees depend on the category of case and are published in the tribunal rules. Professional fees vary with complexity, document volume and the level of representation you choose. Before proceeding, it is sensible to obtain an estimate and weigh this against the tax and penalties at stake.

Q7. What happens if the tribunal denies permission for a late appeal?

If permission is refused, the underlying HMRC decision generally remains final and enforceable. There may be limited scope to appeal the refusal to the Upper Tribunal, but only on a point of law and not simply because you disagree with the outcome. In most cases, a refusal means that litigation routes are effectively exhausted and attention must turn to managing payment and any enforcement.

Q8. Can I settle with HMRC instead of appealing?

Yes. Settlement is often possible, especially where both sides accept that there is some litigation risk. Even if you are pursuing a late appeal, you can usually explore settlement in parallel. HMRC will not always agree to a reduction, but a realistic proposal that reflects legal uncertainty and the costs of further litigation may be considered, particularly in complex or high value cases.

ACT PROMPTLY

Please note that if you have been warned about your file being passed to HMRC’s Solicitor’s Office or have been served a statutory demand or winding-up petition do not delay in taking legal advice. Your matter can be handled more effectively the sooner you contact us.

This guide is intended to provide a clear and practical overview of the law and strategy surrounding late HMRC tax tribunal appeals in the wake of Medpro and the re evaluation of Martland. It is not a substitute for advice on your specific circumstances.